Five Pillars for a CO2-Free Industry in Europe and Italy

Five Pillars for a CO2-Free Industry in Europe and Italy

Nicolò Sartori*

The President of the European Commission Ursula von der Leyen (UvdL) assigned the ambitious task of implementing a European Green Deal to Vice President Timmermans, a key pillar of the new Commission’s policy proposals.[1]

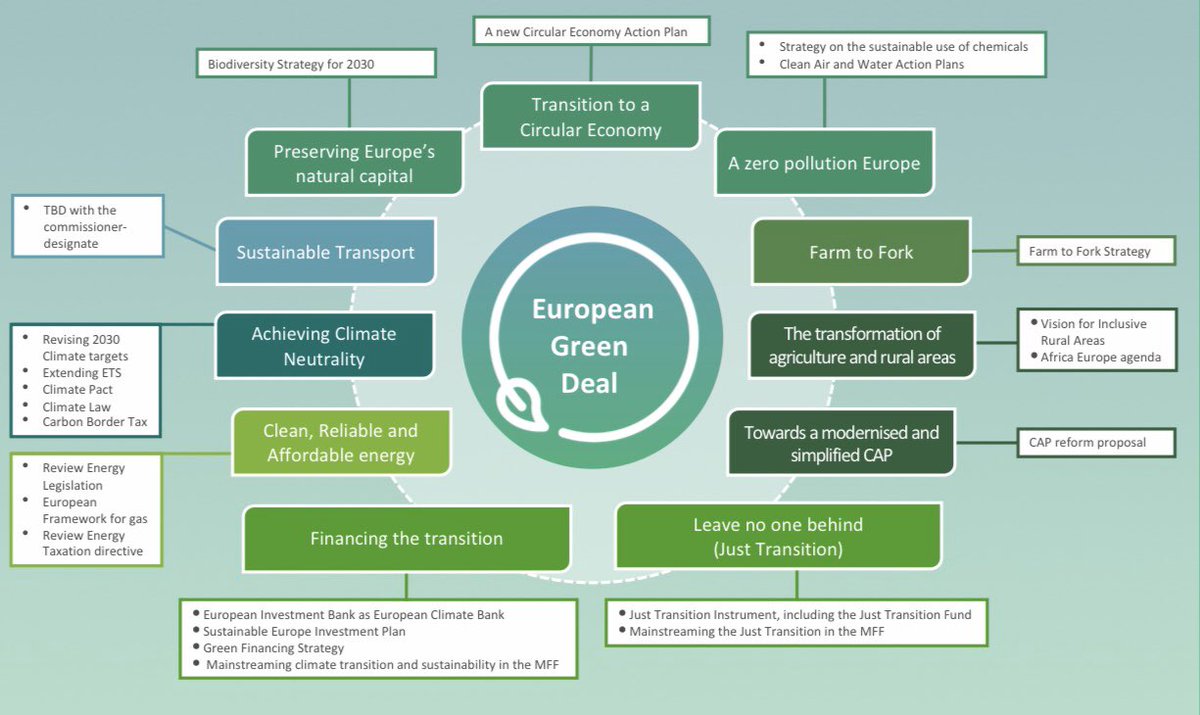

Guided by the goal of becoming the first climate-neutral continent by 2050 (if not before), Timmermans’s efforts – which include the recent presentation of his first programmatic outline (see Figure 1) – will encompass a wide range of sectors, from trade to agriculture, from transport to the blue economy, with significant impact on the habits and way of life of EU citizens.

However, the key element of this Copernican revolution – and one that is surprisingly absent from the Timmermans proposal and the recent Climate Decree approved by the Italian government – is the transformation of the industrial sector, where the effects of a green conversion can be disruptive, in both in positive and negative ways.

Figure 1 | European Green Deal: objectives and proposed measures

Source: Frans Timmermans, Twitter post, 8 October 2019, https://twitter.com/TimmermansEU/status/1181653669399400448.

The industrial sector accounts for approximately one quarter of Europe’s the gross domestic product. Despite trends of de-industrialisation, de-localisation and reconversion towards the tertiary sector now underway in Europe, industry still employs around 50 million people across the continent.

One of the existential challenges for European industry is to maintain its competitiveness among international actors that enjoy significant advantages in terms of wage, environmental and social constraints. The idea of an Industry 4.0 – focussed on automation and the integration of digital technologies to increase productivity, upgrade the quality of facilities and create new business models – goes in this direction.[2] This approach now seems somehow outdated, however. At the very least it has been downgraded to an ancillary position in the more complex transformation process needed for European industry to comply with the climate-neutral trajectory outlined by the new Commission.

To maintain its competitiveness on the global arena, the industry needs to improve its production performance, while aligning – or, better, becoming instrumental – to the complete decarbonisation that the EU is striving for by 2050.[3] The sector – which includes industrial, manufacturing and construction processes – contributes to about 20 per cent of total CO2 emissions in Europe, behind the energy (27 per cent) and transport sectors (24 per cent). Together with the latter, it is among the most difficult and complex sectors to decarbonise (due mainly to energy density issues), whereas on the energy front the massive penetration of renewables makes the reduction of emissions easier to achieve.

With regards to the specific needs of the industrial sector in Europe, the transformation towards more sustainable models of production promised by UvdL’s Green Deal needs to be based on five key pillars: efficiency, decarbonisation, circularity, digitalisation and reconversion.

To promote efficiency means making industrial processes less energy-intensive. This process, where the EU holds a leading role, has already begun. However, there are large margins for improvement – increases in energy efficiency can cut fuel consumption for energy use by 15 to 20 per cent across sectors – especially for the energy-intensive industry.

This opportunity should be fully exploited to reduce consumption and costs while increasing competitiveness. While energy efficiency improvements can competitively reduce carbon footprints, they cannot lead to zero-emissions on their own.

This aspect is intrinsically linked to the need for a coherent and sustainable decarbonisation approach. European industry will embark on a process of reducing CO2 emissions, mainly focused on the electrification of heat, thanks to the usage of furnaces, boilers and heat pumps that run on renewable electricity.[4] However, when electrification options are not viable, it is necessary to develop zero-carbon alternatives.

In this respect, the expansion and use of “green” gases such as hydrogen and biogas is one of the most promising options for European industrial policy. For this to succeed, large investments will be needed to deliver a sustainable (both environmentally and economically) transition for the sector.

The third pillar, circularity, covers processes such as recycling, reusing and converting resources derived from waste materials and by-products used either in industrial processes themselves or from other activities. These processes are another cornerstone of the transformation of European industries. Increasing the circularity of products does not only contribute to improved efficiency and lower operational costs, but can also help cut final CO2 emissions by reducing the production of new materials. The circularity of industrial processes also has an energy dimension, as the biofuels mentioned above are generally the result of recycling and transformation activities.

As foreseen by the concept of Industry 4.0, digitalisation, together with automation, represents one of the main drivers of the future industrial transformation. Connectivity and innovative technologies, including artificial intelligence, clouding, sensors and analytics are cutting-edge instruments the European industry must invest in to reduce inefficiencies, improve the quality of its products and enable new levers of competitive advantage.

Finally, since such transformations, while no doubt positive, will inevitably create winners and losers among citizens, firms and regions, the fifth pillar of reconversion emerges as a key objective to mitigate potential side effects of these processes. Such effects include increased poverty or social exclusion, or indeed that fear of such repercussions effectively slow or constrain reform. In this context, the objectives of reconversion must be the result of prior analyses and planning done by industrial players in partnership with public institutions and civil society, in order to back a just and equitable transition for all.

European industry will need to face huge transformations in order to meet EU decarbonisation targets without losing competitiveness on the global stage. In this context, technological innovation is the key to make industrial processes, applications and products fit for the challenges that lay ahead.

Implementing a significant share of these transformations will necessarily involve the private sector, with policy makers at the European and national level called upon to enable these changes though public policies and support. In this sense, in addition to strategic guidance and policy direction, public funding will play a fundamental role in supporting such industrial conversion processes across Europe.

Action should include investments in R&D&D&D (research, development, demonstration and deployment); direct and indirect financing mechanisms (i.e. loans and incentives and reliefs and deductions respectively). They should further ensure broader and better access to credit for virtuous companies; streamlining authorisation processes for investors in CO2-free industrial applications/processes and a strengthening of carbon-pricing mechanisms, including the adoption of innovative schemes (i.e. carbon border tax).

As we are presently in the initial stages of this transformation, the European Commission’s vision requires a solid financial commitment. The proposed “Sustainable Europe Investment Plan”[5] should aim to meet this objective, avoiding unnecessary and harmful duplications in terms of initiatives and funding (i.e. with the InvestEU programme), but providing clear direction to decarbonisation efforts (at all levels) in the industrial sector. The Plan should be flanked by a more ambitious EU effort on fiscal and taxation policies, led by the Italian Commissioner Paolo Gentiloni, aimed at incentivising member states to adopt a positive approach to foster low-carbon transformations at the national level.[6]

In this transformative context, Italy can and should play a pivotal role. Italy is the second largest manufacturing country in the EU after Germany, and for this reason can expect significant impact by changes affecting the industrial sector (as well as by possible inaction in this domain). Moreover, Italy is already at the forefront when it comes to achievements in energy efficiency (in general, and specifically in the industrial domain) and it is also among EU leaders in efforts to enhance the electrification of energy consumptions thanks to an ambitious (though costly) approach on renewable energy sources (RES) penetration.

Also notable are Italian commitments in the bio-gases sector – it is developing an interesting plan to speed up the deployment of “green hydrogen”. This can become one of the cornerstones for the decarbonisation of industrial processes, and has already set out a digitalisation/automatisation strategy through the National Industry 4.0 Plan strategy launched in 2017 (albeit currently on hold).[7]

Based on these premises, an effective partnership between the Italian government (which already embraced the necessity of a national Green Deal) and the private sector, exploiting the pivotal role of Gentiloni in Brussels to foster a triangulating with the EU, can make Italy emerge as one of the leading European countries driving these transformations that lay ahead.

* Nicolò Sartori is Head of the Energy, Climate & Resources Programme at the Istituto Affari Internazionali (IAI) and Adjunct Professor in “Natural Resources and Energy Security” at the School of International Studies, University of Trento.

This article was previously published in Italian as: “Clima: Ue, cinque regole per un’industria europea CO2-free”, in AffarInternazionali, 21 October 2019, https://www.affarinternazionali.it/?p=75948.

[1] Ursula von der Leyen, Mission Letter to Frans Timmermans, 10 September 2019, https://ec.europa.eu/commission/sites/beta-political/files/mission-letter-frans-timmermans-2019_en.pdf.

[2] See the European Commission DG Growth website: Digital Transformation Monitor, https://ec.europa.eu/growth/tools-databases/dem/monitor/tags/industry-40.

[3] Sam Morgan, “EU Leaders to Back Carbon Neutrality ‘by 2050’, Come Up Short on Final Deal”, in EURACTIV, 20 June 2019, https://www.euractiv.com/section/climate-strategy-2050/news/eu-leaders-to-back-carbon-neutrality-by-2050-come-up-short-on-final-deal.

[4] Eurelectric, Decarbonisation Pathways. Full Study Results, Brussels, November 2018, p. 18, https://www.eurelectric.org/decarbonisation-pathways.

[5] Ursula von der Leyen, A Union That Strives for More. My Agenda for Europe. Political Guidelines for the Next European Commission 2019-2024, 16 July 2019, p. 6, https://ec.europa.eu/commission/sites/beta-political/files/political-guidelines-next-commission_en.pdf.

[6] Ursula von der Leyen, Mission Letter to Paolo Gentiloni, 10 September 2019, p. 5, https://ec.europa.eu/commission/sites/beta-political/files/mission-letter-paolo-gentiloni_en.pdf.

[7] Italian Ministry of Economic Development, National Industry 4.0 Plan (Impresa 4.0), March 2018, http://www.mise.gov.it/index.php/en/202-news-english/2036690.

-

Dati bibliografici

Roma, IAI, ottobre 2019, 5 p. -

In:

-

Numero

19|60